Cathie Wood’s Bitcoin bull thesis concedes stablecoins won the real-world payment fight

Cathie Wood built ARK Invest’s Bitcoin case on the idea that Bitcoin would become a global monetary layer that is programmable, borderless, resistant to inflation, and eventually dominant in payments.

The latest version of that argument concedes that stablecoins got there first on the payments side.

In a recent interview with The Rollup, the ARK CEO said stablecoins have taken over part of the role that ARK once expected Bitcoin to fill in emerging-market payments. At the same time, ETF-era institutions appear to be averaging down during drawdowns, softening the boom-bust severity that defined prior cycles.

Actual stablecoin payments run at roughly $390 billion annualized per McKinsey and Artemis, about 0.02% of global payments volume. Stablecoins have absorbed much of crypto’s transactional lane in the markets where Bitcoin once competed for that role.

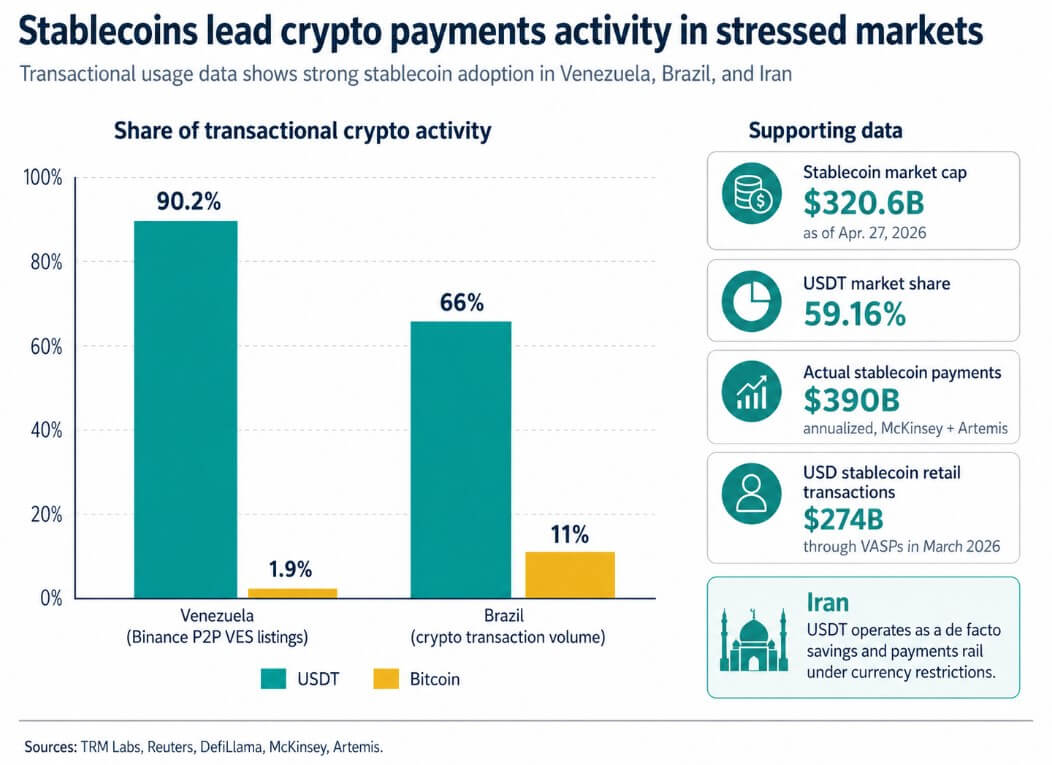

DefiLlama data shows that the stablecoin market cap is over $320.6 billion as of Apr. 27, up over 56% since early 2025, with USDT commanding 59.16% of the market.

TRM Labs’ first-quarter adoption report found that Venezuela’s retail crypto activity primarily runs on stablecoins, with USDT accounting for 90.2% of active Binance P2P Venezuelan bolivar listings and Bitcoin at 1.9%.

In Brazil, roughly 66% of crypto transaction volume was conducted via USDT, with Bitcoin at 11%, and officials noted that stablecoins functioned mainly as payment instruments.

TRM found a similar pattern in Iran, where USDT operates as a de facto savings and payments rail under currency restrictions. The stablecoins pegged to the US dollar processed $274 billion in retail transactions through virtual asset service providers in March 2026 alone.

The payments lane Wood once saw as Bitcoin’s future is now stablecoin infrastructure, and the data in stressed, capital-constrained markets makes that case most clearly.

Bitcoin’s new lane

What stablecoins left behind for Bitcoin is arguably the better seat. As stablecoins absorbed the transactional utility argument, Bitcoin consolidated around scarcity, institutional allocation, and macro reserve positioning.

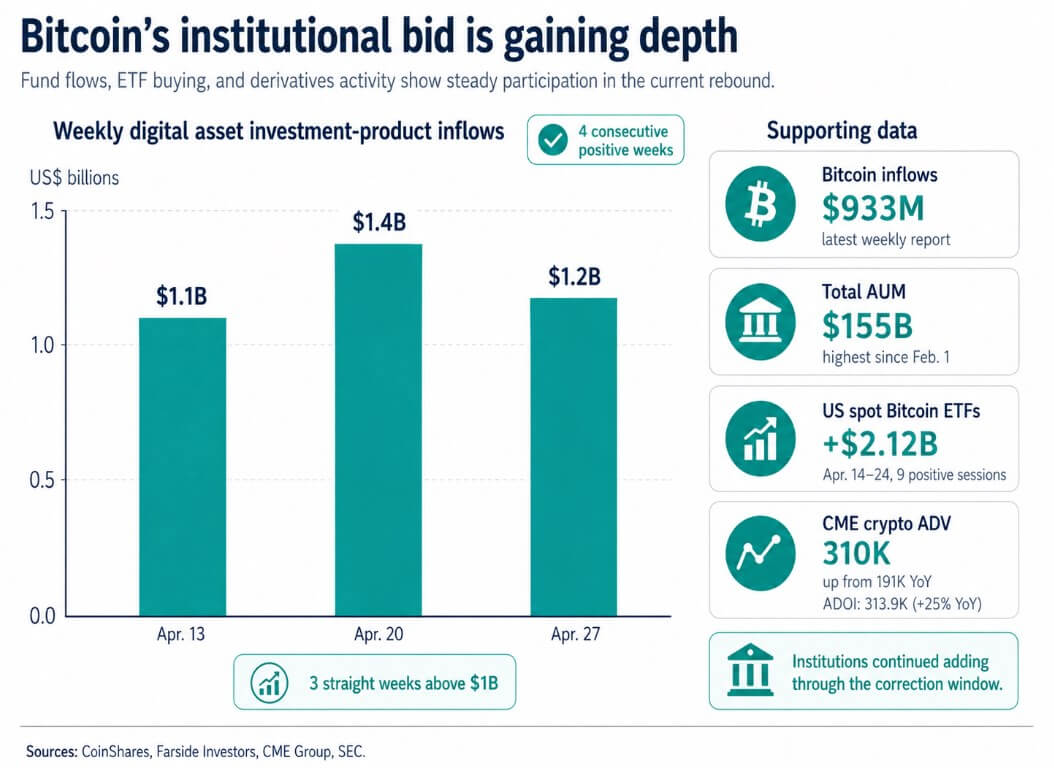

CoinShares’ latest weekly report recorded $1.2 billion in crypto investment product inflows, the fourth consecutive positive week and the third straight above $1 billion.

Bitcoin took $933 million of that total, Ethereum $192 million, and Solana $31.8 million. Total assets under management climbed to $155 billion, the highest reading since Feb. 1.

At the same time, Strategy’s Apr. 27 SEC filing shows another 3,273 BTC purchased during Apr. 20-26, bringing its total to 818,334 BTC at an aggregate cost of $61.8 billion.

CME reported its crypto average daily volume rose from 191,000 to 310,000 contracts year over year in the first quarter, while average daily open interest rose 25% to 313,900 contracts from last year’s first quarter.

Farside Investors’ daily ETF data provide the clearest picture of Wood’s “averaging down” thesis in practice, as US spot Bitcoin ETFs posted nine consecutive positive sessions from Apr. 14 to Apr. 24, with inflows totaling over $2 billion.

Institutions bought through the correction, held through the volatility, and kept adding. Wood’s argument that ETF holders are stickier has that nine-session stretch behind it.

The cycle question

Wood’s thesis runs ahead of its evidence on the possibility that institutions have fully reshaped the four-year cycle.

NYDIG’s research placed retail at 74% of spot Bitcoin ETF AUM as of the fourth quarter of 2024, with institutions and professional advisors at 26%, an expanding share, though still a minority of ownership.

NYDIG’s February 2026 note also argued that Bitcoin’s recent drawdown still fit a cyclical pattern, even if it looked more orderly.

The ETF era has made the marginal buyer more institutional and more macro-responsive, while retail still generates enough selling volume through drawdowns to drive cyclical moves.

Glassnode’s Apr. 22 report adds the market structure layer, noting that Bitcoin reclaimed the True Market Mean at $78,100, with the short-term holder cost basis at $80,100 as the immediate resistance ceiling.

ETF flows turned modestly positive again, and spot demand showed an early recovery, despite short-term holders’ realized profits spiking to $4.4 million per hour, nearly three times the $1.5 million threshold that marked prior local tops this year.

Glassnode also noted that Binance’s cumulative volume delta led much of the recent spot buying while Coinbase activity stayed muted. Since Coinbase proxies US institutional spot demand most directly, the current bid is genuine, driven more by offshore and mid-tier flows.

Two cases

The bull case for Wood’s thesis runs through the Fed.

If the Apr. 28-29 FOMC meeting passes without adding fresh macro stress, weekly inflows hold near or above $1 billion, Coinbase spot participation closes the gap with offshore venues, and Bitcoin clears $80,100 with consistent absorption behind it, Wood’s “institutions softening the cycle” argument becomes visible in price structure.

A market that absorbs $4.4 million per hour in realized profit without breaking the reclaimed mean would exhibit exactly the demand depth Wood describes.

ARK’s published model projects roughly $710,000 in the base case and $1.5 million in the bull case for Bitcoin by 2030, targets that hold only if the institutional ownership thesis compounds across multiple cycles.

The bear case preserves the four-year cycle. If the Fed re-tightens financial conditions, the weekly flow streak breaks, and Glassnode’s realized-profit warning plays out at $80,100, the recent move resolves as a distribution rally.

NYDIG’s view that the market stays cyclical, that retail still owns most of the ETF float, and that the cycle’s boom-bust mechanics stay stronger than institutional depth can currently get the better of Wood’s framing.

Stablecoins would still have won the payments lane, but the halving cycle retains its grip on price structure, with ownership composition playing a secondary role.

Total AUM at $155 billion is 41% below the October 2025 peak of $263 billion, indicating that a large volume of unwound institutional exposure sits above current levels.

| Scenario | What happens | Key signals | What it means for Bitcoin | What it means for Wood’s thesis |

|---|---|---|---|---|

| Bull case | The Fed passes without adding fresh macro stress, the recent demand rebuild holds, and Bitcoin absorbs profit-taking near resistance | Weekly crypto investment-product inflows stay near or above $1B; Coinbase spot participation closes the gap with offshore venues; Bitcoin clears $80,100 with consistent absorption; realized profits stay elevated without breaking the reclaimed mean | Bitcoin shifts from a “rally on trial” to a more durable institutional-demand regime, with ownership mix starting to matter more than the old halving reflex | Supports Wood’s argument that institutions are softening the cycle and that ETF-era buyers are stickier than prior-cycle retail holders |

| Base case | The Fed is broadly neutral, stablecoins keep winning the payments lane, and Bitcoin demand stays positive but uneven | Weekly inflows remain positive but choppy; ETF demand stays constructive but not explosive; Bitcoin holds above $78,100 but struggles to decisively clear $80,100; offshore and mid-tier demand remain stronger than Coinbase-led institutional spot buying | Bitcoin remains supported by macro and institutional flows, but price structure still looks transitional rather than fully reset | Partially validates Wood: the thesis split is real, but institutions have not yet fully reshaped the cycle |

| Bear case | The Fed tightens conditions at the margin, the flow streak breaks, and elevated profit-taking turns the rebound into distribution | Weekly inflows fall back below the recent streak; Glassnode’s realized-profit warning plays out near $80,100; Bitcoin loses support at $78,100; ETF demand fades; retail selling pressure dominates again | The market reverts to a more familiar cyclical pattern, with ownership composition still secondary to drawdown dynamics | Favors NYDIG’s view over Wood’s: stablecoins may have taken payments, but institutions have not yet taken the cycle |

| Structural split outcome | Regardless of short-term price action, stablecoins keep dominating transactional usage while Bitcoin remains the reserve-style asset | Stablecoin market cap stays above $320B; USDT keeps dominant share in stressed payment markets; Bitcoin products continue to capture the bulk of institutional allocation flows | Crypto’s “money” thesis becomes specialized: stablecoins handle payments, Bitcoin handles scarcity and balance-sheet demand | Reinforces Wood’s most durable contribution: Bitcoin did not lose its thesis, it narrowed into a cleaner institutional and reserve-asset role |

What the split actually means

Wood’s most durable contribution to the current debate is the argument that Bitcoin’s original monetary ambition was divided.

Stablecoins became the working dollar rail in capital-constrained markets, while Bitcoin became the scarcer, harder-to-access asset that institutional balance sheets and regulated products hold at scale.

That division is cleaner and may prove more defensible.

Bitcoin can justify a $710,000 base case price on reserve asset and institutional allocation grounds alone.

The stablecoin layer, by absorbing the transactional utility case, leaves Bitcoin with fewer competing demands on its identity, cleaner store-of-value positioning, and a payments infrastructure that keeps capital circulating in crypto without requiring Bitcoin to serve every role at once.

The Apr. 28-29 Fed decision will tell the market if the institutional bid that has rebuilt over four weeks can absorb what Glassnode is already calling elevated profit-taking.