Britain’s bond scare is reopening a question Bitcoin was built for – moments when trust in sovereign debt and monetary management starts to crack.

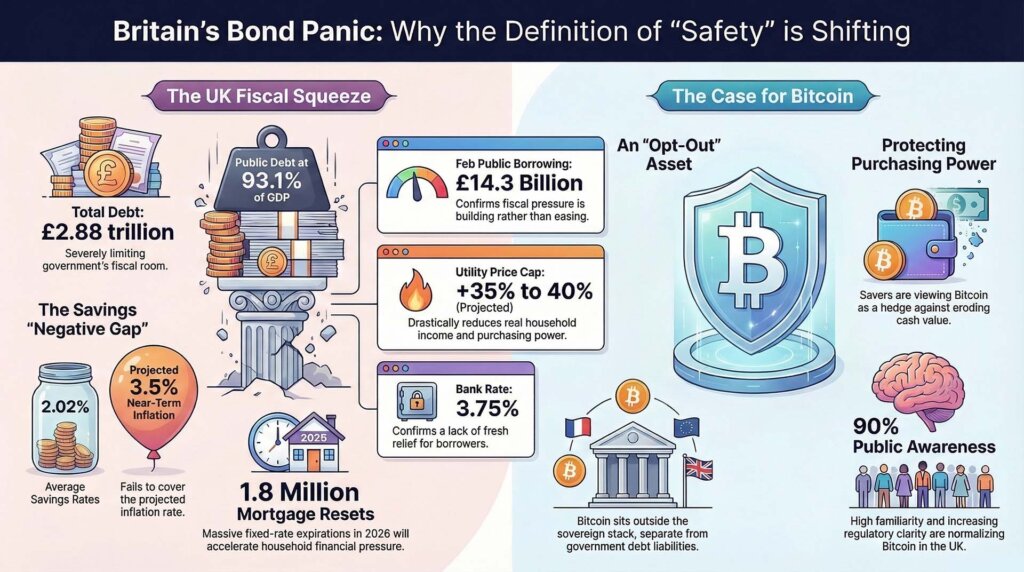

Britain’s fiscal squeeze turned sharper after official borrowing data showed February public sector net borrowing hit £14.3 billion, up £2.2 billion from a year earlier and the second-highest February reading since records began in 1993.

Public sector net debt stood at £2.88 trillion, or 93.1% of GDP. On the same day, the Bank of England held the Bank Rate at 3.75% and warned that the latest energy shock would push inflation back up over the next couple of quarters while raising household fuel and utility costs.

The immediate market response sits in gilts, rate expectations, and mortgages. The slower shift shows up in savings behavior. Britain does not need a rush into Bitcoin for the asset to enter the conversation in a new way. A fresh round of doubt about cash, government bonds, and delayed rate cuts is enough to change how savers rank risk.

That shift starts with arithmetic rather than ideology. The Bank of England said in its latest minutes that preliminary staff estimates now put CPI inflation between 3% and 3.5% over the next couple of quarters. It also said higher household fuel and utility costs would squeeze real incomes. By January, the central bank’s own data showed the average rate on household instant-access deposits at 2.02%.

Easy-access cash is therefore paying less than the inflation range the Bank itself now expects. The gap is plain, about 0.98 to 1.48 percentage points below the near-term CPI path. For savers, that is where the definition of safety starts to shift. Cash still protects nominal value. It does less to protect purchasing power.

Britain’s household channel is also moving quickly. The latest forecast from UK Finance estimates that about 1.8 million fixed-rate mortgages will end in 2026. The Office for National Statistics already showed in its household-costs index that inflation was running at 3.6% for all households and 3.7% for mortgagors in the fourth quarter of 2025. That came before the Bank’s latest warning that energy prices would push costs higher again.

The UK sequence runs through government borrowing, gilt repricing, and household budgets. Gilts look less calm. Easy-access cash runs below the near-term inflation path. Mortgage pain is set to hit more households as fixed deals expire.

Bitcoin gains relevance in that setting as savers consider whether a small asset outside the sovereign stack should be included in the mix.

| Indicator | Latest figure | How it changes saver behavior |

|---|---|---|

| February public borrowing | £14.3 billion | Shows fiscal pressure is still building rather than easing |

| Public debt | 93.1% of GDP | Limits room for a clean fiscal reset |

| Bank Rate | 3.75% | Confirms the Bank did not deliver fresh relief |

| BoE near-term CPI view | 3% to 3.5% | Points to renewed pressure on real incomes |

| Instant-access deposit rate | 2.02% | Leaves easy cash below the Bank’s inflation range |

| Mortgages resetting in 2026 | 1.8 million | Speeds up the household effect of higher rates |

The squeeze starts with cash flow, then reaches portfolio choices

The Bank of England’s latest account of the shock gives the cross-market backdrop. In its March statement, the Bank highlighted that around one-fifth of global oil and LNG supply normally passes through the Strait of Hormuz, Brent crude and Dutch TTF gas prices were about 60% above pre-shock levels, and that UK gas futures implied the next Ofgem cap could rise by 35% to 40%.

That is the bridge between the macro data and the retail saver. A government can run a large deficit for years without changing how households think about money. However, a jump in utility bills lands every month. A mortgage reset lands with a letter and a direct debit. Those are the moments when a saver starts comparing trade-offs across purchasing power, liquidity, volatility, and trust in the issuer.

The distinction is useful as Bitcoin fell about 50% from October 2025 to February 2026, while options volatility climbed to its highest level since 2022. During an active squeeze, investors still sell volatile assets and raise cash. Bitcoin remains sensitive to liquidity stress in those periods.

That pattern also strengthens the longer Bitcoin case in this UK move. Gilts are volatile, expected rate cuts have moved further out, and easy-access cash yields less than the inflation the central bank now expects. Under those conditions, Bitcoin starts to look less like a pure speculation and more like an opt-out from sovereign monetary promises. It carries its own volatility and offers a different source of risk than the one now confronting cash and government debt holders.

The regulatory setup in the UK makes that discussion easier to have than it was a few years ago. The Financial Conduct Authority’s latest consumer research found crypto awareness above 90%, and 25% of crypto users said they would be more likely to invest if the market were more regulated.

The finding supports familiarity with the asset class and sensitivity to regulatory clarity. It leaves the size and timing of any new demand open.

Britain deserves attention outside the UK because the household mechanism is unusually visible. The US still dominates crypto flows, ETF headlines, and dollar liquidity. Yet, Britain shows the pressure points more quickly.

When debt is high, borrowing surprises on the upside, utility bills rise, and a large block of mortgages heads for reset, the question reaches the kitchen table faster. The crypto implication is a broader willingness to treat sovereign paper and bank deposits as incomplete answers to the word “safe.”

The official forecasts point in the same direction. In its March outlook, the OBR projected 10-year gilt yields at 4.5% and 30-year yields at 5.3% before this latest shock, while also seeing public sector net debt rising from 94.5% of GDP in 2025-26 to 96.5% in 2028-29.

It expects the tax burden to rise toward 38% of GDP by 2030-31. Those figures point to sustained fiscal strain and leave little room for a comforting version of the old playbook in which rate cuts, calm bonds, and patient savers solve the problem together.

What the next 12 months could look like

The plausible paths for next year each have a different effect on savings behavior.

The shock fades but does not reverse

The Bank’s 3% to 3.5% inflation range proves roughly right for the next couple of quarters, utility bills rise, and households rebuild precautionary cash even though real returns stay soft.

In that version, Bitcoin may not attract large flows, though it gains narrative ground. The case is simple: if cash is liquid but losing purchasing power, and bonds are no longer calm, a non-sovereign asset looks easier to justify as part of a broader savings mix.

The energy shock persists

The National Institute of Economic and Social Research modeled a persistent-shock scenario in which UK inflation runs 0.7 percentage points higher in 2026, GDP comes in 0.2% lower in 2026 and 0.3% lower in 2027, and Bank Rate ends up about 0.8 percentage points above baseline.

Before the latest move, NIESR’s winter forecast had Bank Rate at 3.25% by the end of 2026. Taken together, those ranges keep a path above 4% in play if the shock sticks.

That is the scenario most likely to deepen the Bitcoin case. High debt narrows fiscal room. Sticky inflation cuts into cash. Higher-for-longer rates hit mortgages. The combination increases interest in assets that sit outside the state’s liabilities, even while Bitcoin itself remains volatile and sensitive to broader market stress.

Market-functioning stress

The third path would hit Bitcoin in the short run and strengthen its appeal over a longer period. NIESR’s separate bond-market note warns that a sovereign duration shock can move from repricing into a financial-stability event, where central banks may need market-functioning support even while inflation is still uncomfortable.

That is the institutional contradiction Bitcoin was designed to answer. It is also the kind of market period that can still pressure Bitcoin first if investors rush for liquidity.

That tension explains why Britain’s latest bond move stands out. The trade is messy. The mechanism is clear. When a state borrows heavily, energy costs rise, inflation firms again, and households face mortgage resets, the social meaning of safety begins to change. The debate moves from macro theory to monthly outflows and preserved purchasing power.

Britain’s latest bond move could become a Bitcoin development before many Americans view it that way.

The UK data already shows the ingredients: £14.3 billion in February borrowing, debt at 93.1% of GDP, a policy rate held at 3.75%, near-term inflation back at 3% to 3.5%, easy-access cash at 2.02%, and 1.8 million mortgages due to reset in 2026.

None of those figures points to an immediate Bitcoin win. Together, they show rising pressure on the old definition of safety.

If energy prices stay elevated, if the next utility cap rises as futures imply, and if mortgage resets keep landing into a period of high gilt yields and delayed rate relief, more savers may decide that cash and government paper no longer answer the whole problem.

")

Leave a Comment